Focused on the Forces That Matter

A Disciplined Approach to Structural Themes

The risk of thematic investing is not that themes are unimportant. It is that they can become powerful drivers of capital allocation and valuation.

Without discipline, that power can lead investors to be too early, too late, or overly confident. When integrated into a structured process, however, themes can illuminate where durable earnings power is forming.

For us, a theme is not a narrative or a trend. It is a structural force shaping the economy — often rooted in a large, pressing problem that must be solved. Companies positioned to address those problems are frequently pursuing substantial market opportunities with the potential for long runways of growth.

But identifying a theme is only the starting point. Without a dynamic framework, themes can mislead as easily as they can inform. Harnessing their power requires a multi-dimensional lens — one that evaluates structural opportunity alongside business quality, valuation, management, and market confirmation.

In the pages that follow, we address some common misconceptions around thematic investing, explain how themes integrate into our multi-perspective process, demonstrate how they help us navigate market transitions, and highlight the structural forces shaping our portfolios today — as well as those beginning to emerge.

Look Up-Before You Look Down

"To me, investing represented a way that people could get ahead if they had a sense of where the world was going."

- Drew Cupps, Head of 5Perspectives Growth Team, Portfolio Manager & Analyst

Over the past 25 years, market leadership has been shaped by a series of powerful structural waves.

In the late 1990s and early 2000s, it was the internet.

In the early to mid-2010s, it was SaaS.

More recently, Generative AI.

Along the way, even seemingly narrow themes — such as the transition to LED lighting — quietly reshaped markets and became ubiquitous across homes, vehicles, and commercial environments.

The lesson is clear: structural themes matter.

In our view, even exceptional stock picking may struggle to sustain outperformance if the forces reshaping the economic landscape are consistently overlooked. The most successful businesses often ride powerful structural tailwinds. Ignoring those tailwinds is not prudence — it is risk.

That is why we look up before we look down.

Before assessing individual companies, we seek to understand the broader structural forces that may amplify — or constrain — their earnings power. Themes do not replace bottom-up analysis. They sharpen it.

From Idea to Investment

Themes inform our process in two critical ways: they guide idea generation and shape how we evaluate every potential investment.

At the earliest stage, themes serve as an organizing lens. They help us step back from individual companies and consider the larger structural forces that may drive inflections in earnings power. Our objective is to identify mispriced growth businesses — but to do so effectively, we must first understand the forces that could amplify or constrain their opportunity

Importantly, identifying a theme does not obligate action. We build thematic “bench strength” by mapping structural problems to companies that appear well positioned to solve them. This stage is about awareness and preparation — so if evidence builds, we are ready.

The decision to invest occurs within our 5Perspectives Attractiveness Evaluation.

Each company is evaluated across five distinct perspectives: valuation upside, business model strength, management quality, thematic power, and technical confirmation. These inputs are synthesized into a single Attractiveness Score — our weight-of-the-evidence framework for allocating capital.

Themes directly influence that score — but not in isolation. A theme may be powerful structurally, yet early in its market recognition. That distinction matters to us. One of the risks of thematic investing is mistiming — being too early, too late, or overstaying once enthusiasm fades.

That is where the technical analysis plays a critical role. Price and volume behavior offer insight into market psychology. When we observe strengthening relative performance across a thematic grouping, it suggests recognition is building. When that behavior deteriorates, it may signal waning enthusiasm.

By integrating thematic conviction with technical discipline, we aim to navigate transitions more smoothly — increasing exposure as structural tailwinds strengthen and market confirmation aligns, and reducing it when evidence weakens.

From the Cloud to the Grid

Market leadership rarely changes overnight. It erodes gradually as capital reallocates and new drivers of growth strengthen beneath the surface. Our objective is to identify those shifts early — before they are fully reflected in prices.

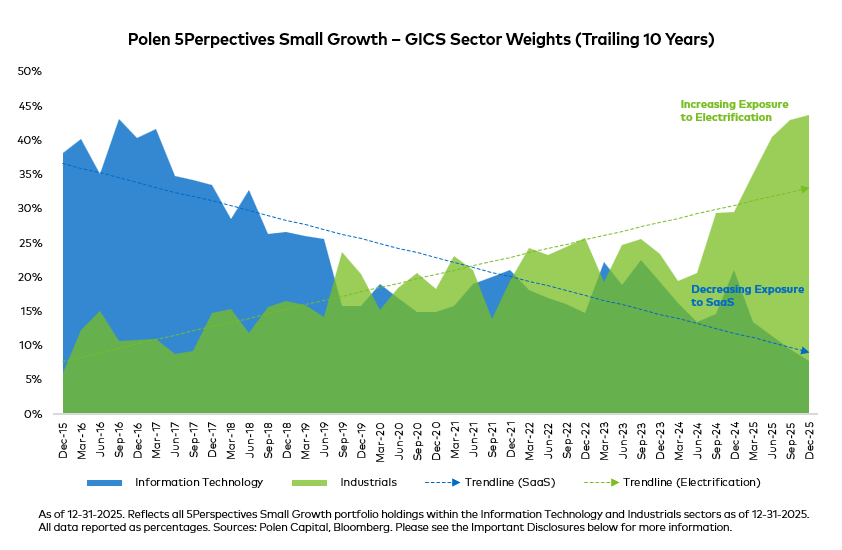

Figure 1 shows how sector exposure evolved within the 5Perspectives Small Growth strategy from 2015 through 2025. While presented at the GICS level, these shifts were driven by bottom-up positioning in specific companies. As exposure to select SaaS businesses declined and Electrification-oriented holdings increased, Information Technology and Industrials weights shifted accordingly.

In the years leading up to 2022, SaaS emerged as a dominant area of market leadership. Accelerating digital transformation, reinforced by the pandemic, met a zero-interest rate environment that amplified revenue growth and drove significant multiple expansion.

At that time, the market rewarded these asset-light, recurring revenue models with sustained price leadership.

As rates reset and growth normalized, that leadership began to fade. Multiples compressed, earnings revisions slowed, and relative strength weakened. Many of these companies remained high quality — but the incremental enthusiasm behind the group diminished.

Our work, however, does not begin with what the market is rewarding.

We focus on structural problems that must be solved. In our opinion, companies positioned to address them often enjoy long runways for growth — whether or not the market has yet fully recognized the opportunity.

Electrification is one such theme for us. We have tracked it since 2005, beginning with the shift toward solar and wind as alternatives to fossil fuels. Over time, its expression evolved: grid reliability became increasingly critical, nuclear re-emerged as a necessary complement, electric vehicles increased power demand, and more recently, data center growth has further strained electricity supply.

The structural issue remained constant: reliable, scalable power is increasingly scarce.

As this imbalance became more visible in earnings revisions and price behavior, we increased exposure to businesses positioned to potentially benefit from electrification. Companies such as Argan, which provides engineering and construction services for power generation facilities; BWX Technologies, a key supplier of nuclear components and fuel; and IES, which supports electrical infrastructure buildouts, reflect that positioning.

We evaluated these businesses within our five-perspective framework, increasing exposure as structural conviction strengthened and market confirmation aligned, and reducing it as leadership faded.

The sector shifts shown in Figure 1 are therefore the outcome — not the starting point — of this process.

"We do not chase narratives. We seek to identify structural problems early and allow evidence to guide capital allocation."

These dynamics are particularly evident today in two areas: the cloud and the grid.

Looking Up - and Ahead

Markets are evolving at an accelerating pace. Structural forces are shifting, leadership is fragmenting, and new drivers of growth are emerging beneath the surface. Our role is to identify those undercurrents early — and reassess them continuously.

Themes are not static allocations. They are living forces that strengthen, mature, and occasionally fade as structural conditions and market psychology evolve. In an environment marked by increasing dispersion between winners and laggards, we think complacency is costly. Discipline is essential.

Artificial Intelligence (AI) is currently the most visible force shaping markets. Yet even within AI, leadership is evolving. In our recent paper, From AI Suppliers to AI Appliers, we explored how the theme is maturing. Early capital concentrated in infrastructure suppliers. As the buildout progresses, we see attention shifting towards companies embedding AI into applications to drive productivity and differentiation.

The theme remains powerful — but its expression appears to be changing.

Figure 1: From Technology to Industrials: A Decade of Evolution

AI’s expansion is also reinforcing our long-standing Electrification theme. Rapid data center growth is accelerating demand for reliable power, intensifying a structural imbalance we have tracked for years. What began as a focus on renewable generation has evolved into a broader challenge of grid stability and scalable electricity supply.

Beyond AI and Electrification, other structural themes continue to shape positioning. Genomics reflects advances in precision medicine. Aerospace is supported by long-cycle demand and defense modernization.

At the same time, we are evaluating emerging undercurrents — including Military 2.0, Space, Housing and consumer recovery, and renewed Biotech innovation. Some are early. Some require clearer evidence. Others may strengthen as conditions shift.

Not every theme becomes a portfolio position. And not every position remains one.

Exposure evolves within the same structured framework — increasing as evidence builds and declining as leadership fades.

Themes evolve. Leadership shifts. Discipline becomes more important, not less.

Discipline Is the Difference

"By combining multiple disciplines into a single view, we aim to see opportunities others may miss and maintain discipline through changing market environments."

- Drew Cupps, Head of 5Perspectives Growth Team, Portfolio Manager & Analyst

We refer to the thematic element of our process as a discipline for a reason. It is not an overlay or a narrative exercise. It is a formal, integrated component of the 5Perspectives framework.

Themes in isolation can mislead. Fundamentals in isolation can miss the broader context. Technicals in isolation can become reactive. When combined, however, we believe they form a more complete view of how earnings power is forming — and when it is being recognized.

By integrating structural insight with business quality, valuation discipline, and market confirmation, we seek to harness the power of themes without becoming captive to them.

In markets shaped by powerful structural forces and accelerating change, we view that discipline as not optional — it is essential.

Important Disclosures

This information has been prepared by Polen Capital without taking into account individual objectives, financial situations or needs. As such, it is for informational purposes only and is not to be relied on as legal, tax, business, investment, accounting, or any other advice. Recipients should seek their own independent financial advice. Investing involves inherent risks, and any particular investment is not suitable for all investors; there is always a risk of losing part or all of your invested capital.

No statement herein should be interpreted as an offer to sell or the solicitation of an offer to buy any security (including, but not limited to, any investment vehicle or separate account managed by Polen Capital). This information is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to local law or regulation.

Unless otherwise stated, any statements and/or information contained herein is as of the date represented above, and the receipt of this information at any time thereafter will not create any implication that the information and/or statements are made as of any subsequent date. Certain information contained herein is derived from third parties beyond Polen Capital’s control or verification and involves significant elements of subjective judgment and analysis. While efforts have been made to ensure the quality and reliability of the information herein, there may be limitations, inaccuracies, or new developments that could impact the accuracy of such information. Therefore, the information contained herein is not guaranteed to be accurate or timely and does not claim to be complete. Polen Capital reserves the right to supplement or amend this content at any time but has no obligation to provide the recipient with any supplemental, amended, replacement or additional information

Any statements made by Polen Capital regarding future events or expectations are forward-looking statements and are based on current assumptions and expectations. Such statements involve inherent risks and uncertainties and are not a reliable indicator of future performance. Actual results may differ materially from those expressed or implied.

References to specific securities, asset classes and financial markets are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations.

As of December 31, 2025, five of the portfolio’s top ten holdings by weight were classified within the Industrials sector. The companies represented herein are included as illustrative examples due to their more direct exposure to electrification themes, including power generation capacity buildout, nuclear energy supply chain participation, and electrical infrastructure and grid support. The other Industrials holdings have broader industrial exposure with less direct alignment to electrification-specific drivers. Past investments and results are not necessarily indicative of any future investments or results. There is no assurance that the securities discussed will be in the portfolio as of the date of this document or that any securities sold have not been repurchased. The securities discussed do not necessarily represent the composite’s entire portfolio. Actual holdings will vary. It should not be assumed that any of the securities transactions or holdings discussed were or will prove to be profitable or that any investment recommendations we make in the future will equal the investment performance of the securities discussed herein. For a complete list of Polen Capital's past specific recommendations holdings and current holdings as of the current quarter end, please contact info@polencapital.com.

The Global Industry Classification Standard (“GICS”) was developed by and is the exclusive property and a service mark of MSCI Inc. (“MSCI”) and Standard & Poor’s, a division of The McGraw-Hill Companies, Inc. (“S&P”) and is licensed for use by Polen Capital Management, LLC. Neither MSCI, S&P nor any third party involved in making or compiling the GICS or any GICS classifications makes any express or implied warranties or representations with respect to such standard or classification (or the results to be obtained by the use thereof), and all such parties hereby expressly disclaim all warranties of originality, accuracy, completeness, merchantability and fitness for a particular purpose with respect to any of such standard or classification. Without limiting any of the foregoing, in no event shall MSCI, S&P, any of their affiliates or any third party involved in making or compiling the GICS or any GICS classifications have any liability for any direct, indirect, special, punitive, consequential or any other damages (including lost profits) even if notified of the possibility of such damages.

The Polen 5Perspectives Small Growth (the “Strategy”) began in November 2000 and was managed by Cupps Capital until October 2016 at which time it was transitioned to Advisory Research Investment Management. In March 2024, it transitioned to Bosun Asset Management, and subsequently in June 2025, it transitioned to Polen Capital. Andrew Cupps has served as the portfolio manager of the Strategy since inception. Mr. Cupps has been supported in his role as portfolio manager by various individuals, including Kevin Leitner and Chris Bush. Mr. Leitner has worked on the Strategy since inception. Mr. Bush began working on the Strategy in 2007. At all times during his tenure as portfolio manager, Mr. Cupps has had ultimate decision-making authority with respect to the Strategy. Mr. Cupps, Mr. Leitner and Mr. Bush joined Polen Capital on June 30, 2025.

This information may not be redistributed and/or reproduced without the prior written permission of Polen Capital.

Connect with Us

For more information on Polen Capital visit www.polencapital.com and connect with us on LinkedIn.