A Section 351 Exchange is a powerful solution for concentrated, low-basis positions, enabling diversification while preserving unrealized gains. At the same time, a 351 exchange can help investors transition managers and modernize legacy portfolios into a potentially more flexible, tax-efficient ETF structure—all without the friction of selling appreciated assets.

Get the Complete 351 Exchange Guide

Is a 351 Exchange Right for You?

Who Benefits Most

- UHNW investors

- Families with large embedded gains

- Clients with concentrated employer or legacy positions

- Advisors serving clients with complex taxable portfolios

The Problem

Concentrated, low-basis positions create compounding challenges, such as:

- Large exposures to a single stock increase portfolio risk

- Selling triggers an immediate tax bill

- Direct indexing and megacap performance amplify unintended overweighting

The Solution

A Section 351 Exchange provides a tax-deferred path to diversify concentrated, low-basis holdings while restoring portfolio alignment—all in one mechanism.

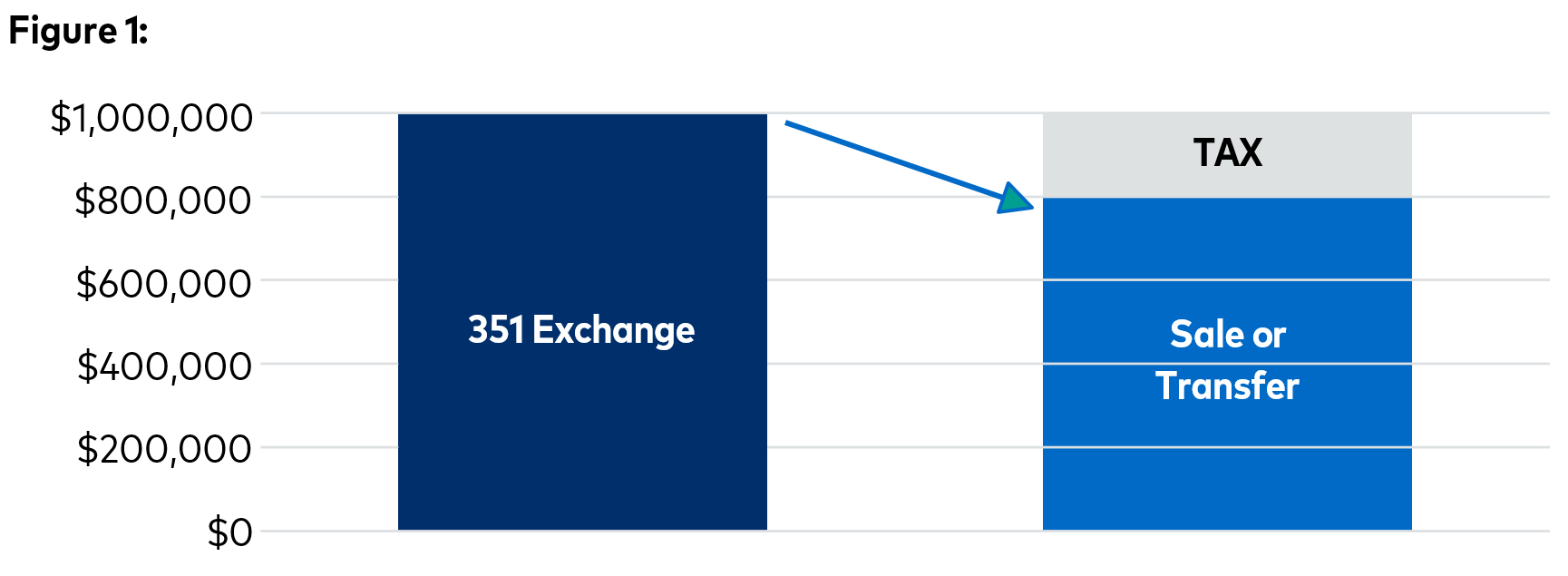

Tax-Free Today vs. Tax-Efficient Tomorrow

Tax-Free Today — Section 351 Exchange

- Transfer appreciated securities without recognizing capital gains at transfer

- Original cost basis and holding period carry over to received ETF shares

- Avoid concentration legacy or concentrated holdings without a taxable event

Assumptions: Long-Term Capital Gains + Net Investment Income Tax Rate: 23.8%.

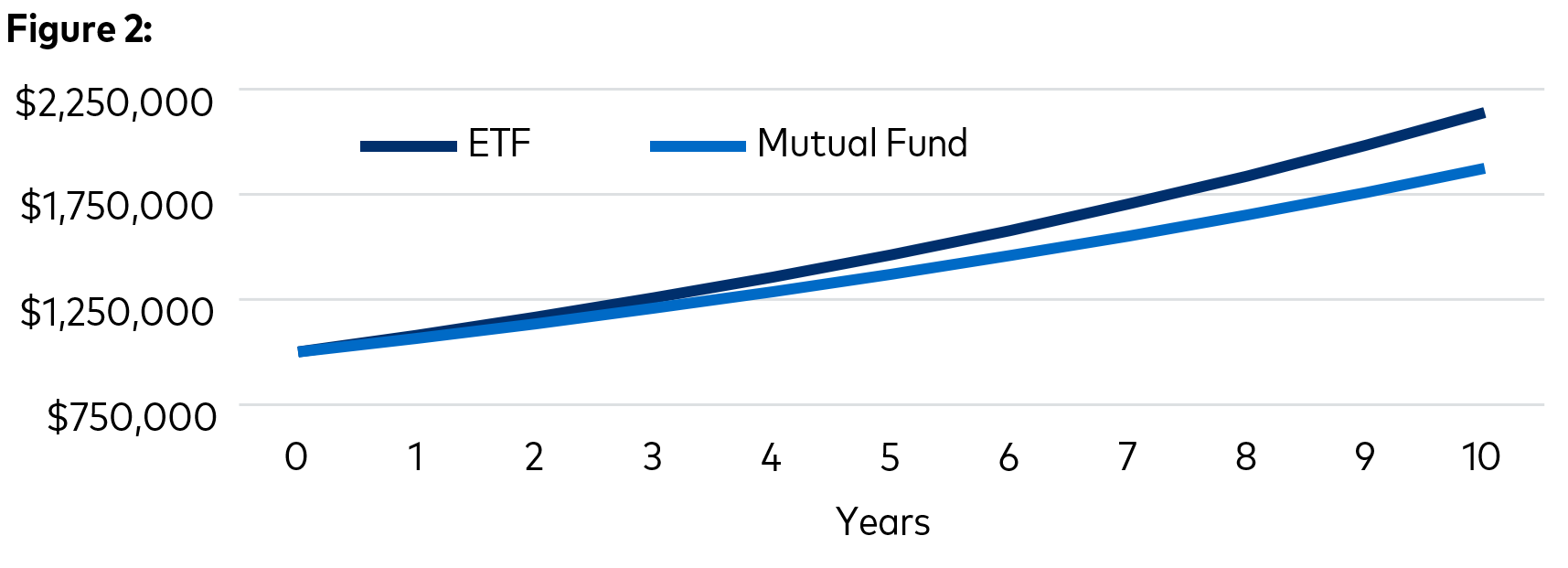

Tax-Efficient Tomorrow — ETF's Continuing Tax Advantages

- In-kind creations and redemptions limit fund-level capital gains and taxable distributions

- Investors control when gains are realized — typically when they sell ETF shares

- ETFs help defer tax drag after-tax compounding over time

Annual gross return for each both vehicle is 8%, ETF annual taxable distribution: 0.5% of NAV, Mutual fund annual taxable distribution: 6% of NAV, Taxes assessed each year on the distribution amount reduce that year’s value (after-tax compounding).

Converting with Confidence: The 351 Timeline

We've designed a clear, step-by-step process to make your 351 Exchange as seamless as possible. Having successfully completed this process last year, we're well-positioned to provide support through each stage.

Step 1: Initial Review

6-8+ weeks before Launch

- Review your current holdings to identify concentrated, low-basis positions

- Discuss your goals with your financial advisor

- Tax Deferral

- Diversification

- Liquidity

- Confirm timing around the upcoming ETF launch

Step 2: Portfolio Assessment

4-6 weeks before Launch

- Submit full holdings file for analysis

- Ensure diversification requirements are met:

- Max 25% in one company

- Max 50% in top five positions

- Identify any adjustments needed

Step 3: Preparation & Documentation

2-4 weeks before Launch

- Finalize necessary agreements

- Coordinate logistics with your custodian

- Confirm eligibility under Section 351 guidelines

- Trading in the portfolio will pause two weeks before launch

Step 4: ETF Launch & Exchange

Launch Date

- Contribute approved securities to the new ETF

- Receive ETF shares at Net Asset Value (NAV)

- Defer capital gains taxes, if requirements are satisfied

Step 5: Ongoing Ownership

Post Launch

- ETF begins trading on the exchange

- Clients maintain liquidity and diversification in their portfolios

- Taxes deferred until ETF shares are sold

What we need from you:

- Custodian LOA: Form authorizing your custodian to transfer shares from your account to the ETF

- Month-end brokerage statement showing tax lots being contributed

- Subscription Agreement

Once eligibility and interested is confirmed we will need:

- An Excel file of holdings including tax lot information, account numbers for each client participating, security identifiers, shares

Everything You Need to Know

We've created comprehensive resources to help you understand the 351 Exchange.

The Concentration Challenge

Diversify. Defer Taxes. Defend Your Gains.

About 351 Exchanges

Paths to Reduce Concentration

The primary strategies investors use

The Tax Tradeoffs

Tax-Free In, Tax-Efficient Within

Preserving Investable capital

Tax-Free Today vs. Tax-Efficient Tomorrow

By the numbers comparison

Evaluating a Section 351 Exchange

From Strategy To Execution

A Simple 3-step process

Implementing the 351 Exchange

Converting with Confidence - The 351 Timeline

- Complete step-by step process

- Required documents checklist

- Key dates and deadlines

How Section 351 Exchanges Affect Taxes

- Detailed 351 Exchange overview

- Requirements and qualifications

- Portfolio examples

From Diversification to Opportunity

- Section 351 exchange diversification overview

- Long-term growth investing framework

- Historical performance and portfolio positioning

- Comparison table

Common Questions

A: Section 351 of the Internal Revenue Code allows investors to transfer appreciated assets into an ETF without triggering capital gains taxes at the time of transfer—similar to a 1031 exchange in real estate. Investors receive ETF shares in exchange for their contributed securities, deferring taxes on unrealized gains.

A: To qualify, your portfolio must meet these criteria:

· No single issuer's securities may exceed 25% of the portfolio's value

· The top five issuers' securities may not exceed 50% of the portfolio's value in total

· Contributed positions must align with the ETF's investment mandate

A: The 351 Exchange window is expected to close this summer. Participation requires advance coordination and documentation, so we recommend starting the conversation as soon as possible.

A: Required documents include:

· Excel file of holdings with tax lot information

· Custodian Letter of Authorization (LOA)

· Month-end brokerage statement

· Subscription Agreement

A: Contact Laura Graff, Head of Product Strategy, at lgraff@polencapital.com or +1 561 645 8862.

Interested in a potential Section 351 exchange into an ETF?

Polen anticipates launching an ETF that is expected to follow the 5Perspective Growth Opportunities strategy. The Growth Opportunities strategy invests in growth companies across all market capitalizations (small-, mid-, and large-cap). Guided by our 5Perspectives framework—a multi-discipline approach refined over nearly 25 years—the strategy is designed to identify exceptional businesses poised to benefit from secular trends.

Ready to explore your options?

Our team is here to answer your questions and determine if a 351 Exchange is right for you and your clients.

Important Disclosures: This information is not to be relied on as legal, tax, business, investment, accounting, or any other advice. Recipients should seek their own independent financial and tax advice. Investing involves inherent risks, and any particular investment is not suitable for all investors; there is always a risk of losing part or all of your invested capital. The information is in a summary format and therefore very limited in scope and not meant to provide comprehensive descriptions or discussions of the topics mentioned herein. Moreover, this has been prepared without taking into account individual objectives, financial situations or needs. As such, this presentation is for informational discussion purposes only. No statement herein should be interpreted as an offer to sell or the solicitation of an offer to buy any security (including, but not limited to, any investment vehicle or separate account managed by Polen Capital). Any timelines referenced herein are provided for illustrative purposes only and may be modified at any time.

This information is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to local law or regulation. Any statements made by Polen Capital regarding future events or expectations are forward-looking statements and are based on current assumptions and expectations. Such statements involve inherent risks and uncertainties and are not a reliable indicator of future performance. Actual results may differ materially from those expressed or implied. References to specific securities, asset classes and financial markets are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations. This information may not be redistributed and/or reproduced without the prior written permission of Polen Capital.