Investing in the Next Phase of Artificial Intelligence

Key Highlights

- We believe that AI will have a transformative impact across nearly every industry in the coming years. Yet, although the long-term market potential is immense, the direction—and pace—of AI's evolution is clouded by possibilities and uncertainties.

- While we expect AI to remain a dominant investment theme, we also believe it is still too early to accurately determine long-term winners and losers, given that many of AI's most significant challenges and opportunities still lie ahead.

- We think the next leg of AI opportunities will broaden and include innovative companies beyond the tech sector. We also see opportunities outside the U.S.—particularly in Europe and Asia—where valuations appear more attractive.

- With momentum dominating equity markets and valuations appearing stretched in certain areas, we do not dismiss the possibility of volatility during the year's second half.

Artificial Intelligence: A Bundle of Possibilities

In recent years, very few developments have captured investors' imagination and curiosity as much as the emergence of generative artificial intelligence (AI). Although its origins trace back to the 1950s, the release of ChatGPT—a consumer-focused AI chatbot and virtual assistant—in late 2022 marked a turning point that sparked a global frenzy around all things AI.

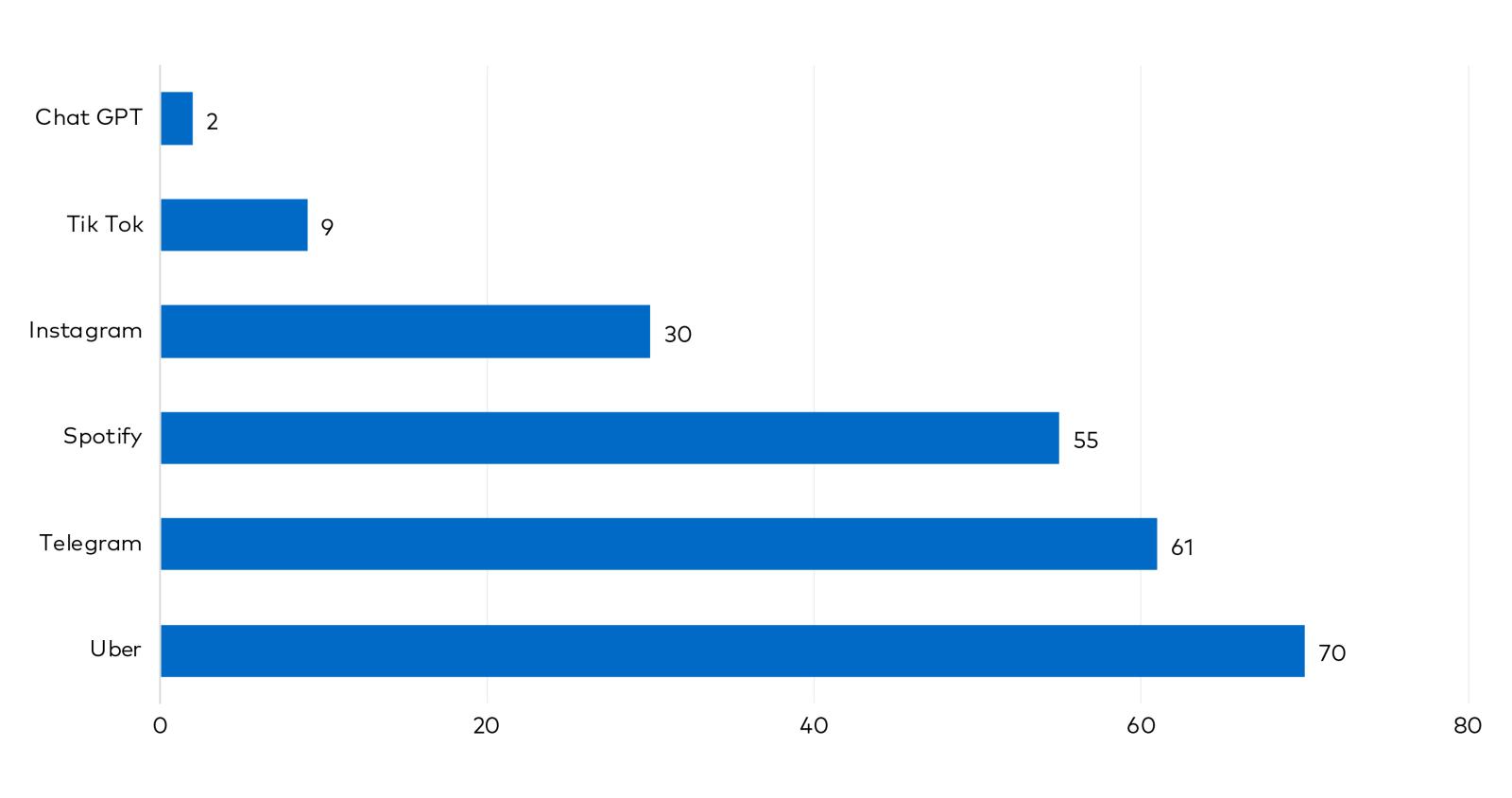

Thanks to its public accessibility and intuitive interface, ChatGPT gained over 100 million active users just two months after launching, as shown in Figure 1. The tool's meteoric rise into one of the fastest-growing applications in history evidences the magnitude of demand for AI technologies and excitement around its transformative potential.

Figure 1: Months to Reach 100 Million Global Users

Source: Bloomberg. As of January 2024.

In simple terms, generative AI uses various technologies to simulate human intelligence and problem-solving capabilities. AI can "learn" from past data to autonomously perform complex tasks like writing software code from scratch and providing accurate answers to user queries.1 In fact, AI has already surpassed human performance in several areas, including image classification, visual reasoning, and English understanding, according to research from Stanford University.2

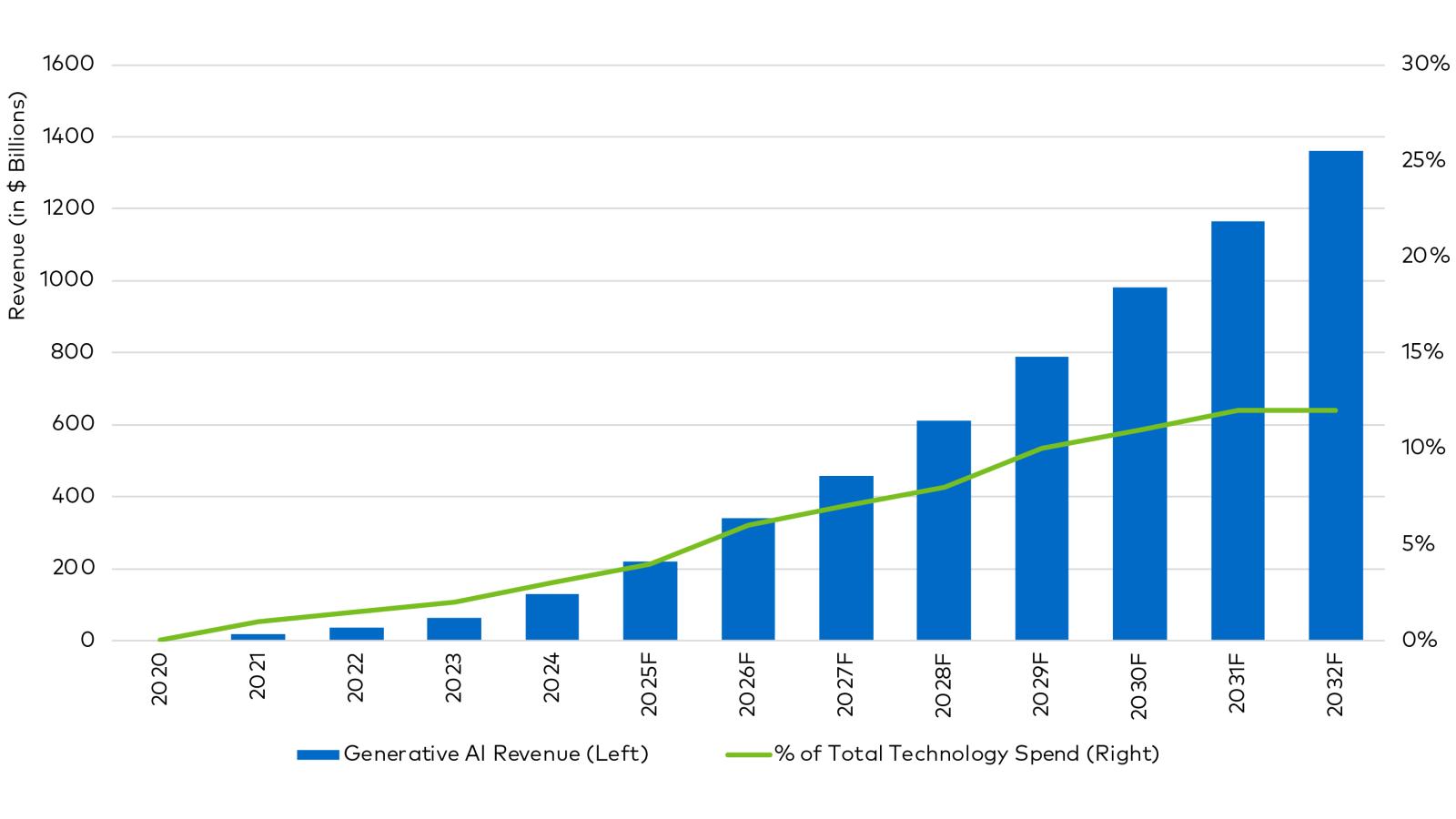

Despite its infancy, different studies have proven that generative AI's ability to model intelligent behaviors can boost business productivity and enhance business performance.3 According to PwC, the sectors most exposed to AI—such as financial services, information technology, and professional services—are seeing productivity gains five times larger than those less exposed to AI.4 Across the technology landscape, businesses have entered an "AI arms race," making substantial investments to build generative AI capabilities to capture a slice of what Bloomberg estimates will become a $1.4 trillion market by 2032 (Figure 2).5

Figure 2: AI Market Growth Forecast

Source: Bloomberg. Most recent estimates were published in June 2024.

The AI Rally: Is There a Bubble Brewing Underneath?

So far this year, ever-increasing momentum around AI propelled global equity indexes to record highs, with mega-cap tech leading the rally. According to Bloomberg, the seven biggest U.S. companies—commonly known as the "Magnificent 7"— saw their combined weighting in the S&P 500 rise to a record 30% as some investors believe they stand at the center of AI adoption and deployment given their vast scale, financial resources, and talent.6 Nevertheless, the rapid pace of the rally has left other investors concerned about frothy valuations drawing similarities with the dot-com boom of the 1990s, which propelled the NASDAQ index—a barometer of the U.S. tech sector—800% higher in just five years, only for it to plunge 78% after the Internet bubble burst in 2000, taking more than 12 years to recover fully.7

Though our research indicates that valuations appear stretched in some areas of the market, we believe today's investment landscape vastly differs from the one seen during the dot-com bubble.8 Unlike the unprofitable tech companies of the 1990s, the latest U.S. earnings season results showed that booming demand for AI adoption has resulted in revenue growth for the companies at the epicenter of AI enablement. Meanwhile, instead of rising along with early leaders, money-losing tech companies have seen their share prices sink this year as investors become increasingly more discerning.9

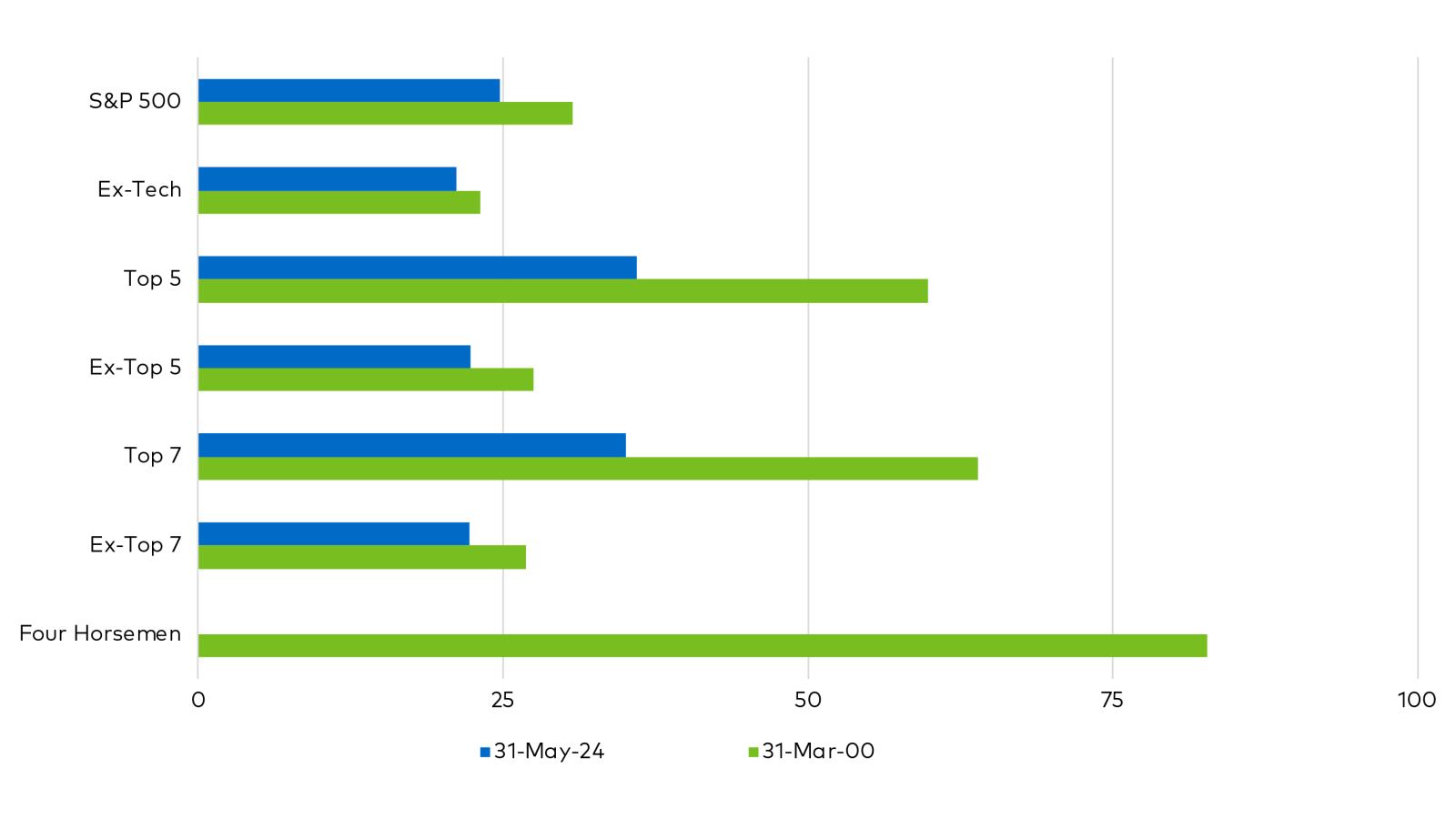

Furthermore, stock valuations are much lower than during the dot-com bubble's peak. Currently, the S&P 500 trades more than five times earnings beneath its 2000 peak cap-weighed P/E, and the largest tech companies trade at nearly half the P/E multiples from the late 1990s tech bubble10. When equities peaked in March 2000, the top 7 ranked by market cap in the S&P 500 traded at 64 times P/E, and the Four Horsemen11 traded at more than 80 times trailing earnings. Today, as seen in Figure 3, the five largest S&P 500 companies trade at a P/E multiple of 36 times, less than half the Four Horsemen's top P/E.12

Figure 3: Trailing Twelve Months P/E Ratios: 2000 Valuations vs. Today

Source: Bloomberg. As of May 28, 2024.

Is It Too Early or Too Late to Invest in AI?

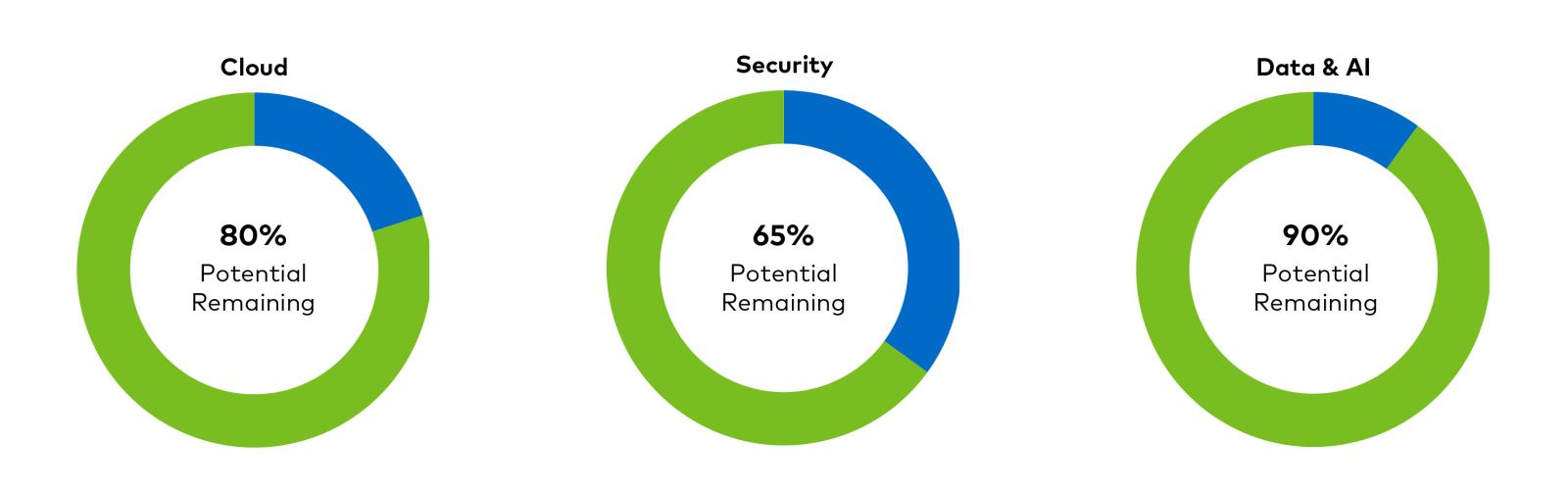

The rapid surge in AI-related stocks has left some market participants questioning whether it's too late to invest in the sector. Despite this year's positive performance, our research indicates AI is still in its early stages, and much uncertainty lingers around issues like governance, ethics, data security and accuracy. As Figure 4 shows, similar to other digital solutions, most of AI's potential remains untapped and not fully understood. Yet, it is essential to remember that a promising narrative does not always necessarily translate into a great investment. Therefore, we believe investors should exercise patience and a long-term mindset when seeking opportunities across the AI innovation cycle.

Figure 4: Untapped Potential of Technology Solutions

Source: Accenture. Study published June 2024.

While many companies have made significant investments in AI, we believe not all will be able to turn expenditures into profits. As we have seen in the past, widespread adoption of technological advances—such as the internet—usually takes time to develop, and market leaders change often and swiftly. For example, according to data compiled by Bloomberg, of the ten best performers in the NASDAQ the year leading up to the index's 2000 peak, only two still exist as standalone companies today.13 Similarly, the companies at the helm of the AI revolution may look different five years from now, with incumbents falling behind competitors or even new companies becoming market leaders.

Investor Takeaways: Look Beyond Today's Winners

Looking forward, we believe AI will pave the way for many compelling investment opportunities over the next decade. However, given that we are still in the early days of AI, we think it is important to resist the fear of missing out driven by the allure of quick gains. Rather than aiming to be the first to hop on a new trend or hot company, we believe that taking our time to truly understand a company's prospects before we invest in it is critical in assessing the sustainability of its competitive advantages.

Even for those businesses leading the AI rally, certain risks loom. For example, NVIDIA14 —which manufactures the chips that power AI systems—reminded investors last month that stocks don't go up forever. The company's shares experienced their worst selloff in four years amid concerns about its ability to sustain its fast pace of revenue growth in the years to come.15 According to our research, the company's valuation could prove expensive if there is a meaningful digestion period following the purchases from its large customers in the past two years.

Also, we believe that investors focusing on just a few U.S. tech companies may be overlooking AI opportunities in other regions. With AI gaining momentum worldwide, domestic champions are rising across Europe and Asia, where valuations are more attractive. For many economies experiencing labor shortages and low productivity growth, AI represents an opportunity for economic development and the creation of new industries entirely. Hence, we suggest investors apply a global lens when exploring AI opportunities, favoring high-quality businesses with proven competitive advantages led by management teams prioritizing long-term performance.16

Despite our constructive outlook, we believe that AI's evolution and growth won't be linear but bumpy as new solutions emerge and the divide grows between winners and losers. With over 30% of the S&P 500's value concentrated in the "Magnificent 7," investors should know that index exposure in today's market does not represent diversification. For passive investors, a sudden shift in expectations of the "Magnificent 7" could result in a sharp correction, particularly when some companies are trading at elevated levels relative to the broader market. This is why we believe employing an active approach in today's environment is essential— looking at each company individually and understanding their unique circumstances and prospects.

Important Disclosures

1 Source: Harvard Business Review. As of June 2023.

2 Source: Standford University 2024 Artificial Intelligence Index Report.

3 Source: University of Oxford. As of September 2023. MIT Sloan. As of December 2023.

4 Source: 2024 PwC Global AI Jobs Barometer.

5 Source: Bloomberg Intelligence. Bloomberg estimates that AI could expand at an annual rate of 42% over the next decade, growing from $137 billion in 2024 to $1.3 trillion by 2032.

6 The “Magnificent Seven” refers to Alphabet, Amazon, Apple, Meta Platforms, Microsoft, Nvidia, and Tesla.

7 Source: Bloomberg.

8 The dot-com bubble was a period between the late 1990s and early 2000s when the stock market saw a rapid increase in the valuations of internet-based companies.

9 Source: Q1 2024 Factset Earnings Insights. As of May 24, 2024.

10 Source: Bloomberg. As of June, 2024. The trailing Price-to-Earnings (P/E) ratio is a relative valuation multiple that is based on the last 12 months of actual earnings.

11 Cisco, Dell, Intel, and Microsoft were referred to as the “Four Horsemen” due to their market leadership during the 1990s.

12 Source: Bloomberg Intelligence Report - Is AI Driving U.S. Tech Bubble 2.0?

13 Qualcomm and Check Point Software Technologies.

14 NVIDIA is not part of any Polen Capital strategy as of June 21, 2024.

15 Source: Bloomberg. Bloomberg Evening Briefing: Wall Street Ends the Week in a ‘Tech Wreck’ - Bloomberg

16 We believe that high-quality companies are those with a durable earnings profile driven by a sustainable competitive advantage, superior financial strength, sound sustainability practices, proven management teams, and powerful products/ services.

This information is provided for illustrative purposes only. Opinions and views expressed constitute the judgment of Polen Capital as of June 2024 and may involve a number of assumptions and estimates that are not guaranteed and are subject to change without notice or update. Although the information and any opinions or views given have been obtained from or based on sources believed to be reliable, no warranty or representation is made as to their correctness, completeness or accuracy.

Opinions, estimates, forecasts, and statements of financial market trends that are based on current market conditions constitute our judgment and are subject to change without notice, including any forward-looking estimates or statements that are based on certain expectations and assumptions. The views and strategies described may not be suitable for all clients.

The price-to-earnings (P/E) ratio measures a company's current share price relative to its per-share earnings. This document does not identify all the risks (direct or indirect) or other considerations which might be material to you when entering any financial transaction. Past performance does not guarantee future results and profitable results cannot be guaranteed.

The information in this document has been prepared without taking into account individual objectives, financial situations or needs. It should not be relied upon as a substitute for financial or other specialist advice. This document is provided on a confidential basis for informational purposes only and may not be reproduced in any form or transmitted to any person without authorization from Polen Capital.