Navigating Credit Risk: Lessons from the First Brands Default

Highlights

First Brands’ well-publicized “freefall” bankruptcy in late September sent ripples through public and private credit markets. While headlines have been painful, the overall effect on the CLO market has been quite limited. In our view, CLO structural and diversification benefits are designed to mitigate the influence of any single credit.

In this note, we highlight:

- What happened leading up to First Brands’ default

- Polen’s 0% exposure to First Brands across credit products

- Our continued conviction in the CLO asset class

What Happened

First Brands Group, a privately held auto parts manufacturer behind brands like TRICO, Autolite, and FRAM, filed for Chapter 11 bankruptcy on September 29th, 2025. The filing revealed a staggering “$10 billion to $50 billion in liabilities against just $1 billion to $10 billion in assets,” making it one of the most significant and opaque defaults in recent memory.

The filing followed a failed attempt by First Brands to refinance its capital structure in July 2025 as lenders’ concerns about its financial transparency grew. The ~$6B refinancing attempt triggered the unraveling of First Brands’ significant off-balance-sheet liabilities.

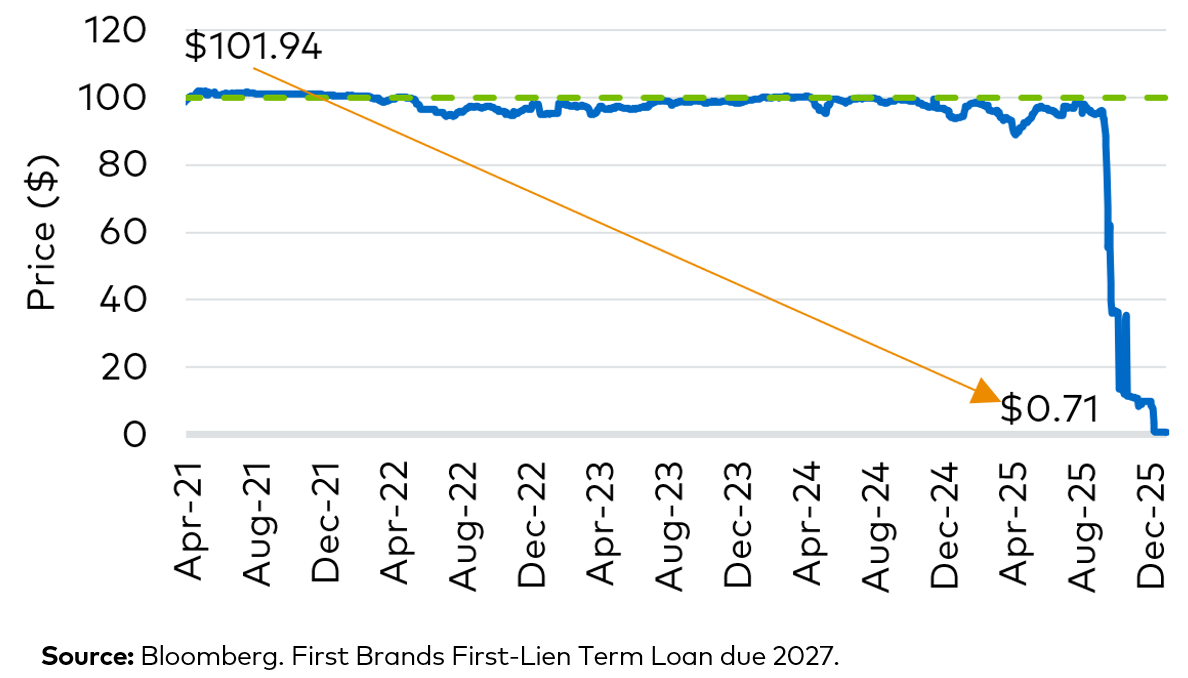

The company’s debt—once trading near par—plummeted, triggering multi-notch downgrades from rating agencies.

First Brands' Loan Price: From Par to Distressed

Aggressive Growth, Hidden Leverage

Based on financial information obtained by Polen during the company's attempted refinancing in July, First Brands was reportedly in a strong financial position generating ~$5.6 billion of revenue, ~$1.9 billion of Adj. EBITDA with net first-lien leverage of 1.9x. This reported profitability allowed the company to pursue a debt-fueled acquisition spree in recent years.

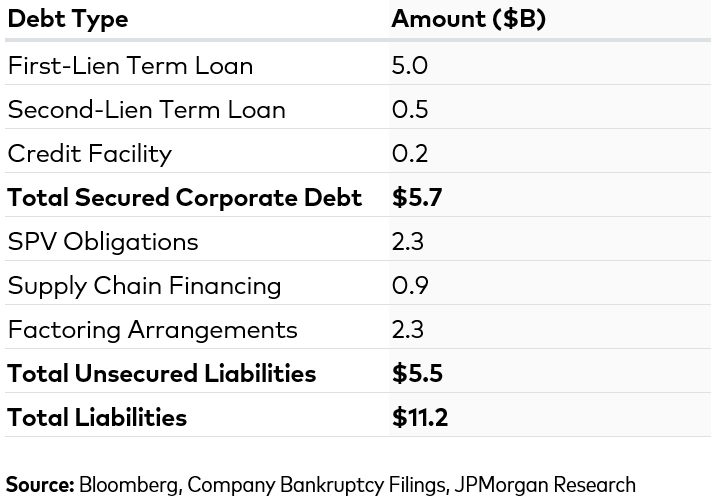

Based on information known today, for years First Brands accessed the broadly syndicated loan market (BSL), raising ~$5.4 billion of on-balance sheet debt. However, its financing efforts were not limited to the BSL market; private lenders were tapped as well.

Unbeknownst to the BSL market, the company borrowed an additional ~$5.5 billion from a variety of private credit providers, including:

- ~$2.3B in inventory-backed deals through opaque special-purpose vehicles (SPVs)

- ~$2.3B of invoice factoring arrangements

- ~$900M via supply chain finance arrangements

Currently, regulators are investigating whether the firm double-pledged its inventory and receivables through off-balance-sheet arrangements with private lenders.

Estimated First Brands Debt Capitalization

Credit Market Jitters

The collapse of First Brands as well as subprime auto lender Tricolor has sent ripples through credit markets—spanning leveraged loans, CLOs, trade-finance funds, and asset-backed auto lending.

Investor Reactions

Leveraged loan funds recorded their largest weekly outflow since April, with $1.3B withdrawn for the week ending October 15. Loan ETFs saw their first outflow in 19 weeks, totaling $1.0B—comprising $186M from CLO ETFs and $846M from loan ETFs.

CLO Exposure

Of First Brands’ ~$5B first-lien senior secured debt, U.S. CLOs hold ~$2.1B (54% of the U.S. dollar tranche), while European CLOs hold €520M of the euro tranche (81%). This represents just 0.2% of overall collateral in both regions – a manageable number. However, the degree across exposed managers varies, and while we view the First Brands default as idiosyncratic, we do anticipate a divergence in CLO equity performance through the next credit cycle.

The collapse of First Brands highlights the importance of performing manager due diligence, including an assessment of credit underwriting quality, as a key area of focus for investors.

Polen Positioning

Exposure

Funds and accounts managed by Polen Capital have never had any exposure to First Brands (or its subsidiaries).

Why We Passed

Our Team spent hours analyzing the company, but never invested due to:

1. Substantial use of unquantifiable off-balance sheet financings

2. M&A history (20 acquisitions in the last 5 years)

3. The company’s evasive and mysterious owner

"Polen holds 0% of First Brands across credit products. We looked at the First Brands deal earlier this year and concluded that it was a hard pass."

- Rick Richert, CLO Portfolio Manager

Important Disclosures

The information in this document is provided for informational purposes only. This document is not intended as a guarantee of profitable outcomes. Past performance is not indicative of future results. The opinions and estimates expressed herein constitute the judgement of Polen Capital as of the date of this document, are not guaranteed, and are subject to change without notice or update, including any forward-looking estimates or statements which are based on certain expectations and assumptions. Although the information and any opinions or views given have been obtained from or based on sources believed to be reliable, no warranty or representation is made as to their correctness, completeness or accuracy. The views and strategies described may not be suitable for all clients. References to specific securities, asset classes and financial markets are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations. This document does not identify all the risks (direct or indirect) or other considerations which might be material when entering into any financial transaction. This information may not be redistributed and/or reproduced without the prior written permission of Polen Capital.

Sources: JPMorgan Global Research, BofA Global Research, Company Filings, Debtwire, Intex, Markit, Deutsche Bank.

Connect with Us

For more information on Polen Capital visit www.polencapital.com and connect with us on LinkedIn.