Why CLO Equity Deserves a Seat at the Table — and Why Sophisticated Investors Have an Edge

In a world where attractive double-digit risk-adjusted yields are increasingly scarce and constant bouts of volatility are the norm, investors are searching for strategies that deliver both resilience and return.

In today’s market, investors face a paradox: the hunt for yield often leads to higher risk, while safety comes at the cost of return. Enter CLO equity — a lesser-known but powerful strategy that sits at the intersection of innovation and income. At its core, CLO equity represents the first-loss tranche in a Collateralized Loan Obligation, a structured credit vehicle backed by a diversified pool of senior secured corporate loans. While CLO equity bears the most risk in the structure, it also captures the highest upside. Historically, that trade-off has delivered strong, risk-adjusted returns for those who understand its mechanics. Yet despite these attributes, CLO equity remains under‑allocated and widely misunderstood.

So why isn’t everyone talking about it? The answer lies in accessibility—and that’s where the conversation gets interesting.

From Niche to Necessary: The Rise of CLOs

To understand why CLO equity matters, investors first need to understand how central CLOs have become to the leveraged loan market. Many investors still view CLOs as a niche corner of structured credit. The market suggests otherwise. The U.S. leveraged loan market now approaches $1.5 trillion. CLOs hold roughly two-thirds of outstanding broadly syndicated corporate loans, making them the single largest source of demand. That scale changes the conversation.

CLO growth has mirrored the expansion of the loan market over the past two decades, reinforcing that CLOs are not cyclical opportunists, but structural participants. While market share has fluctuated across cycles, CLOs have remained central to the system — and today represent its dominant buyer base. Put simply: the modern leveraged loan market depends on CLOs.

At this scale and level of integration, CLOs are not a tactical allocation. They are embedded in the infrastructure of corporate credit. If CLOs form the backbone of this market, the question becomes how investors should access them.

Why CLO Equity Belongs in Portfolios

CLO equity offers a compelling combination of benefits that make it a valuable addition to diversified portfolios:

-

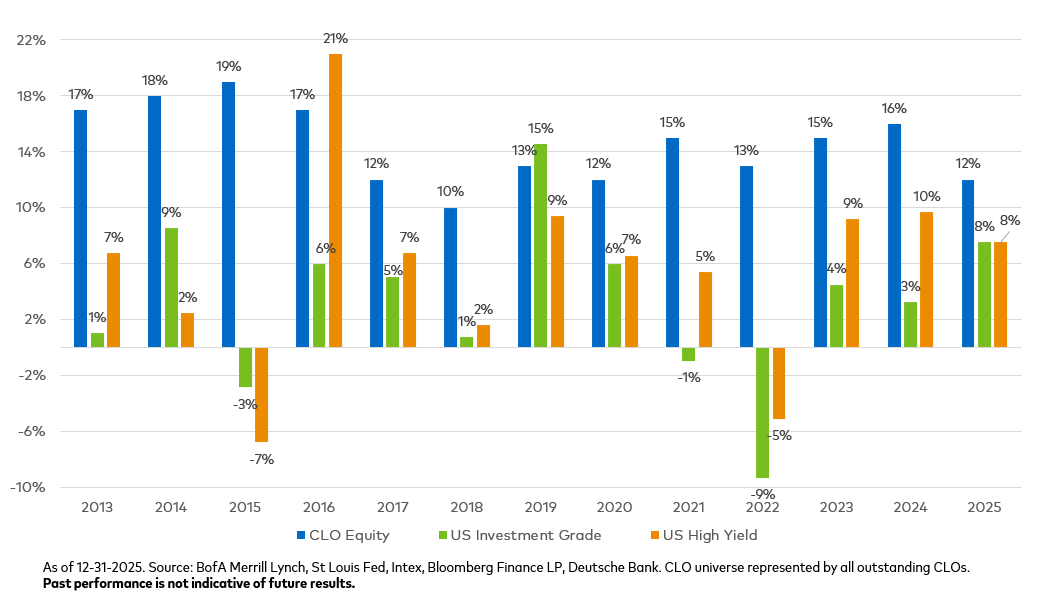

High Yield Potential: Historically, CLO equity has delivered returns far exceeding traditional fixed income. In a world where high-quality bonds yield 4–6%, that difference is hard to ignore — a point clearly demonstrated below.

Figure 1: CLO Equity Has Delivered Higher IRRs Than Traditional Fixed Income (2013-2015)

- Front-loaded, durable, and predictable cash distributions: CLO equity tranches begin paying quarterly income shortly after a deal has closed. Historically, distributions have landed in the mid-teens annually - providing reliable cash flow without a private-equity-style J-curve.

- Diversification: CLO equity provides exposure to a diversified pool of senior secured bank loans, an asset class that has historically exhibited low correlation to both equities and traditional fixed income. This structural diversification can help mitigate portfolio concentration and improve overall risk-adjusted outcomes.

- Lower Volatility than Equities: CLOs are actively managed vehicles with reinvestment periods and built-in credit enhancement features. Managers can trade loans, adjust risk exposures, and optimize portfolios over time - capabilities not typically available in traditional passive bond portfolios.

- Strong Underlying Credit Quality: Loan portfolios within CLOs have historically demonstrated stronger credit performance than the broader leveraged credit market, reinforcing the asset class's resilience and contributing more consistent long-term results.

CLO equity's structural complexity and limited liquidity can deter many investors. For sophisticated allocators, however, these same characteristics can provide access to an illiquidity and complexity premium that more conventional strategies cannot replicate.

These advantages explain why CLO equity deserves a seat at the table - and why the real question for investors is not whether it belongs, but how to access it.

This excerpt introduces the case for CLO equity.

For a deeper examination of performance history, portfolio construction considerations, and access pathways, download the full paper below.

Important Disclosures

This information has been prepared by Polen Capital without taking into account individual objectives, financial situations or needs. As such, it is for informational purposes only and is not to be relied on as legal, tax, business, investment, accounting, or any other advice. Recipients should seek their own independent financial advice. Investing involves inherent risks, and any particular investment is not suitable for all investors; there is always a risk of losing part or all of your invested capital.

No statement herein should be interpreted as an offer to sell or the solicitation of an offer to buy any security (including, but not limited to, any investment vehicle or separate account managed by Polen Capital). This information is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to local law or regulation.

Unless otherwise stated, any statements and/or information contained herein is as of the date represented above, and the receipt of this information at any time thereafter will not create any implication that the information and/or statements are made as of any subsequent date. Certain information contained herein is derived from third parties beyond Polen Capital’s control or verification and involves significant elements of subjective judgment and analysis. While efforts have been made to ensure the quality and reliability of the information herein, there may be limitations, inaccuracies, or new developments that could impact the accuracy of such information. Therefore, the information contained herein is not guaranteed to be accurate or timely and does not claim to be complete. Polen Capital reserves the right to supplement or amend this content at any time but has no obligation to provide the recipient with any supplemental, amended, replacement or additional information.

Any statements made by Polen Capital regarding future events or expectations are forward-looking statements and are based on current assumptions and expectations. Such statements involve inherent risks and uncertainties and are not a reliable indicator of future performance. Actual results may differ materially from those expressed or implied.

References to specific securities, asset classes and financial markets are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations.

This information may not be redistributed and/or reproduced without the prior written permission of Polen Capital.

Definitions:

Correlation measures the degree to which two variables move in relation to each other, expressed on a scale from –1 to +1. A positive correlation means they move in the same direction, a negative correlation means they move in opposite directions, and a correlation near zero indicates little to no linear relationship. Internal Rate of Return (IRR) is the annualized rate of return that makes the present value of an investment’s future cash flows equal to its initial investment, reflecting both the timing and magnitude of cash flows. J‑curve describes the tendency for certain investments, especially private market or closed‑end structures, to show negative returns early on before rising to stronger positive returns over time. Early drawdowns reflect upfront costs or delayed cash flows, while later periods capture value creation or income generation. The S&P 500 Index, which is maintained by S&P Dow Jones Indices, is a market capitalization weighted index that measures 500 common equities that are generally representative of the U.S. stock market. The performance of an index does not reflect any transaction costs, management fees, or taxes.

Connect with Us

For more information on Polen Capital visit www.polencapital.com and connect with us on LinkedIn.